What's happening to UK interest rates and what does it mean?

Getty Images

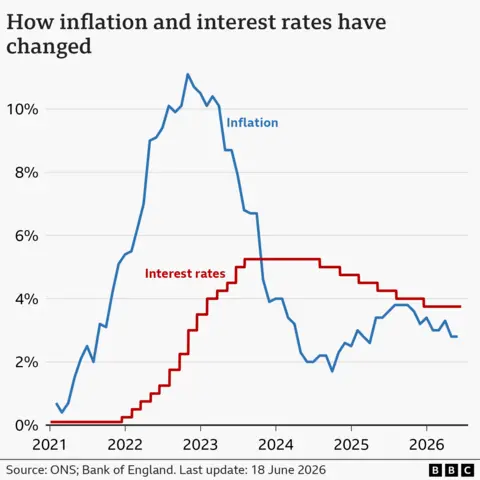

Getty ImagesThe Bank of England has held interest rates at 3.75% for a fourth consecutive time, keeping them at the lowest level since February 2023.

Rates dropped from 4% in December 2025, and further cuts had been expected in 2026, but the economic impact of the war in Iran means many analysts believe no cuts are likely for the rest of the year.

Interest rates affect mortgage, credit card and savings rates for millions of people.

What are interest rates and why do they change?

An interest rate tells you how much it costs to borrow money, or the reward for saving it.

The Bank of England's base rate is what it charges other banks and building societies to borrow money, which influences what they charge their own customers for mortgages as well as the interest rate they pay on savings.

The Bank moves its benchmark rate up and down in order to keep UK inflation - the rate at which prices are increasing - at or near 2%.

When inflation is above that target, the Bank typically puts rates up. The idea is to encourage people to spend less, reducing demand for goods and services and limiting price rises.

What has been happening to UK interest rates and inflation?

The main UK inflation measure, CPI, has dropped significantly since the high of 11.1% recorded in October 2022 as a result of the war in Ukraine.

It was 2.8% in the year to May 2026, unchanged from the previous month.

The Office for National Statistics (ONS), which tracks UK inflation, said inflation remained steady because while transport costs rose by the fastest rate since December 2022, that increase was offset by a slowing in the pace of price rises for food.

The US-Israel war with Iran has put up energy and fuel costs around the world and is expected to increase the pace of price rises more generally.

The Bank of England's base rate reached a recent high of 5.25% in 2023. It remained at that level until August 2024, when the Bank started cutting.

Five cuts brought rates down to 4%, before the Bank held rates at its meetings in September and November 2025, before the December cut and further holds in January, March, April and June 2026.

Could UK interest rates go up?

The Bank had been widely expected to cut interest rates twice in 2026, with the first drop predicted to come in March or April.

However, the increase in fuel prices and inflation after the outbreak of the US-Israeli war with Iran has upended all of this.

Analysts are guarded about likely moves for the rest of the year but a wait and see approach is dominant among policymakers.

Sustained higher inflation could push rates up, but the weakness of the UK's jobs market and sluggish economic growth in general means this is by no means certain.

Oil prices have fallen sharply after the US and Iran agreed a deal to end the war.

Bank of England governor Andrew Bailey said on 18 June that the recent falls were "encouraging".

However, he added: "Whatever happens in the future, the higher energy prices of the past four months mean there's already some inflationary pressure in the pipeline.

"The Bank's job is to make sure that doesn't turn into sustained inflation above our 2% target."

How do interest rate cuts affect mortgages, loans and savings rates?

Getty Images

Getty ImagesMortgages

Just under a third of households have a mortgage, according to the government's English Housing Survey.

About 500,000 homeowners have a mortgage that "tracks" the Bank of England's rate. That means any cut means a reduction in the monthly repayments on their outstanding loan.

An additional 500,000 homeowners on standard variable (SVR) rates rely on their lender choosing to pass on any Bank rate cut.

But the vast majority of mortgage customers - some 87% - have fixed-rate deals. While their monthly payments aren't immediately affected by a rate change, their future deals are.

As of 18 June, the average rate on a new two-year fixed deal was 5.59%, up from 4.83% at the start of March, according to the financial information service Moneyfacts.

For those looking for a five-year deal, the average rate was 5.57%, up from 4.95% over the same period.

The average two-year tracker rate was 4.48%.

About 800,000 fixed-rate mortgages with an interest rate of 3% or below are expected to expire every year, on average, until the end of 2027. Borrowing costs for customers coming off those deals are likely to rise sharply.

Mortgage calculator

You can see how your mortgage may be affected by future interest rate changes by using our calculator:

Credit cards and loans

Bank of England interest rates also influence the amount charged on credit cards, bank loans and car loans.

Lenders can decide to reduce their own interest rates if Bank cuts make borrowing costs cheaper.

However, this tends to happen very slowly.

Getty Images

Getty ImagesSavings

The Bank base rate also affects how much savers earn on their money.

A falling base rate is likely to mean a reduction in the returns offered to savers by banks and building societies and vice versa.

As of 17 June, Moneyfacts said the average rate for an easy access savings account was 2.53%.

Any cut in rates could particularly affect those who rely on the interest from their savings to top up their income.

What is happening to interest rates in other countries?

In recent years, the UK has had one of the highest interest rates in the G7 - the group representing the world's seven largest so-called "advanced" economies.

In June 2024, the European Central Bank (ECB) started to cut its main interest rate for the eurozone from an all-time high of 4%, until it reached 2% in June 2025.

However, in June 2026, the ECB raised rates to 2.25% as it reacted to rising prices triggered by the Iran war.

The US central bank - the Federal Reserve - has cut interest rates three times since September 2025, taking them to the current range of 3.5% to 3.75%, the lowest since 2022.

The Fed voted to hold rates at that level at its most recent meeting on 17 June.

President Trump had repeatedly attacked the Fed, and its then chairman Jerome Powell for not cutting rates earlier. Powell has now been replaced by Kevin Warsh who is expected to be more supportive of further cuts.

However, the most recent inflation data showed that US prices rose in May at their fastest annual rate for three years.