UK borrowing costs jump as uncertainty over PM's future continues

Getty Images

Getty ImagesGovernment borrowing costs jumped on Tuesday amid uncertainty over the future of Prime Minister Sir Keir Starmer.

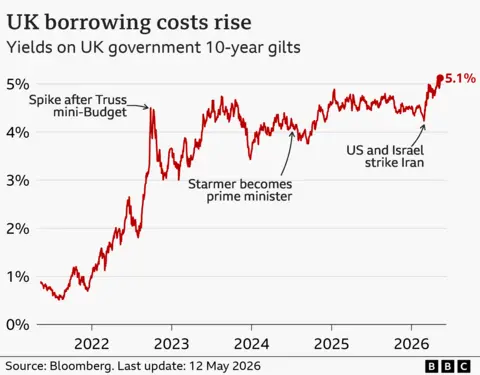

The effective interest rate on borrowing over 10 years briefly hit a high of 5.13%, near levels last seen during the 2008 global financial crisis.

Financial markets have been on edge due to fears higher oil prices caused by the Iran war will push up inflation and lead to interest rate hikes.

But the possibility of a change of leadership in the UK and perceived risk of looser public spending has further unsettled investors.

The UK's main stock index, the FTSE 100, fell more than 1% in opening trade but later closed down just 0.04%.

Shares in banks including Lloyds, NatWest and Barclays all fell amid concerns of a tax raid by a potential new administration. The pound also fell 0.5% against the dollar to $1.35.

While all governments have seen borrowing costs rise since the Iran war sent oil prices soaring above $100 a barrel, the UK has experienced elevated rates compared to countries with economies similar in size.

The risk that potential replacements for Sir Keir might loosen public spending and increase borrowing by the government is concerning investors, analysts said.

The prime minister and Chancellor Rachel Reeves have consistently committed to "iron clad" rules on borrowing in a bid to reassure markets their economic plans are credible.

But some Labour MPs on the left of the party have questioned whether the UK's budget rules were "fit for long-term renewal".

Analysts at Capital Economics said they believed UK borrowing costs would rise and the pound would weaken if there was a change at the top of the Labour party.

"The UK's already fragile fiscal position means that investors will be on edge for any signs of fiscal loosening," they said.

"The likely replacements for Starmer/Reeves would probably not be as fiscally disciplined."

They suggested all the frontrunners to potentially challenge Sir Keir - Andy Burnham, Angela Rayner and Wes Streeting - would "probably raise public spending".

Anna Macdonald, investment strategy director at Hargreaves Lansdown, said the bond market had been "frazzled" by concerns a different prime minister might take a different view on borrowing, "relaxing fiscal rules or extending them".

"This would mean that investors, of which 25-30% are overseas buyers of UK government bonds, demand a higher risk premium," she added.

Governments get most of their income from taxes, but often want to spend more money than taxes raise.

To cover that gap, they borrow money from investors and issue something called a bond or gilt, which is a loan the government promises to pay back at the end of an agreed term.

But when investors lend to governments, they want a degree of certainty and confidence that they will get their money back. If they perceive the loan as more risky, they will demand a higher rate of return.

On Tuesday, borrowing costs - as shown by the bond yield, or interest rate - across two, five, 10 and 30-year terms were all higher as the prime minister's future was in peril. The yield on 30-year bonds hit 5.81%, the highest since 1998.

The 10-year gilt is the benchmark for government bonds, while the two and five-year gilts have an influence on fixed-rate mortgage rates of the same time frame.

While the effective interest rate on UK borrowing rose on Thursday, the increase was slightly higher than rises seen for the French and German governments. The jump in inflationary expectations caused by the surge in energy costs since the Iran war began has been the main driver of higher borrowing costs globally in recent weeks.

The amount of interest the government pays on existing public debt is linked to inflation and the interest rates on bonds. The sum has been rising in recent years and now accounts for about £1 in every £10 the government spends.